Equity rally stalls but catches breadth on positive earnings

Key Observations

- U.S. equity returns were mixed after a strong December rally while the Treasury curve steepened as investors bet that policymakers would swiftly pass a new $1.9 trillion stimulus package.

- Corporate earnings are set to rebound strong in 2021 which may be supportive of incremental gains despite elevated valuations.

- While we are generally constructive on markets in the near-term, we will be keenly focused on the rebound in business activity following more progress with the vaccine.

Market Recap

Despite entering 2021 with elevated long-term valuations, near term financial market conditions remained favorable for risk assets. Georgia’s special election results cemented Democrat control of the Senate and cleared a path for President Biden’s $1.9 trillion stimulus plan. In the wake of COVID-19, coordinated fiscal and monetary policy will likely support economic growth and result in strong corporate earnings growth in 2021. That said, asset class returns were mixed in January.

Within Fixed Income, higher inflation expectations steepened the U.S. Treasury yield curve which more than offset lower credit spreads. The Bloomberg Barclays Aggregate Index fell 0.7 percent (1). U.S. Equity returns were bifurcated as small caps outperformed large caps. Overall, the S&P 500 Index fell 1 percent while the Russell 2000 Index (a proxy for small-cap stocks) rallied 5 percent (2). International equities were similarly mixed. The MSCI EAFE fell 1.1 percent, but emerging market stocks (those most sensitive to a rebound in global economic growth and represented by the MSCI EM Index) returned 3.1 percent (3).

Rising inflation expectations supported higher commodity prices collectively, but accelerated growth trends detracted from returns on precious metals specifically. Real assets most sensitive to fluctuations in global growth trends such as energy produced strong returns, while U.S. REITs returned 0.1 percent (4).

Corporate Benefits

Conditions remain favorable for economic growth to accelerate in the first half of the year as vaccine distribution efforts improve and permit economic normalization. Despite elevated equity valuations entering 2021, the combined effect of the Fed’s purchase program ($120 billion per month) and a fresh round of fiscal stimulus ($1.9 trillion) should stoke household consumption in the near-term and produce strong year-over-year earnings growth. In our view, the combination of joint stimulus measures and reopening underpin the recently increased breadth of asset class returns.

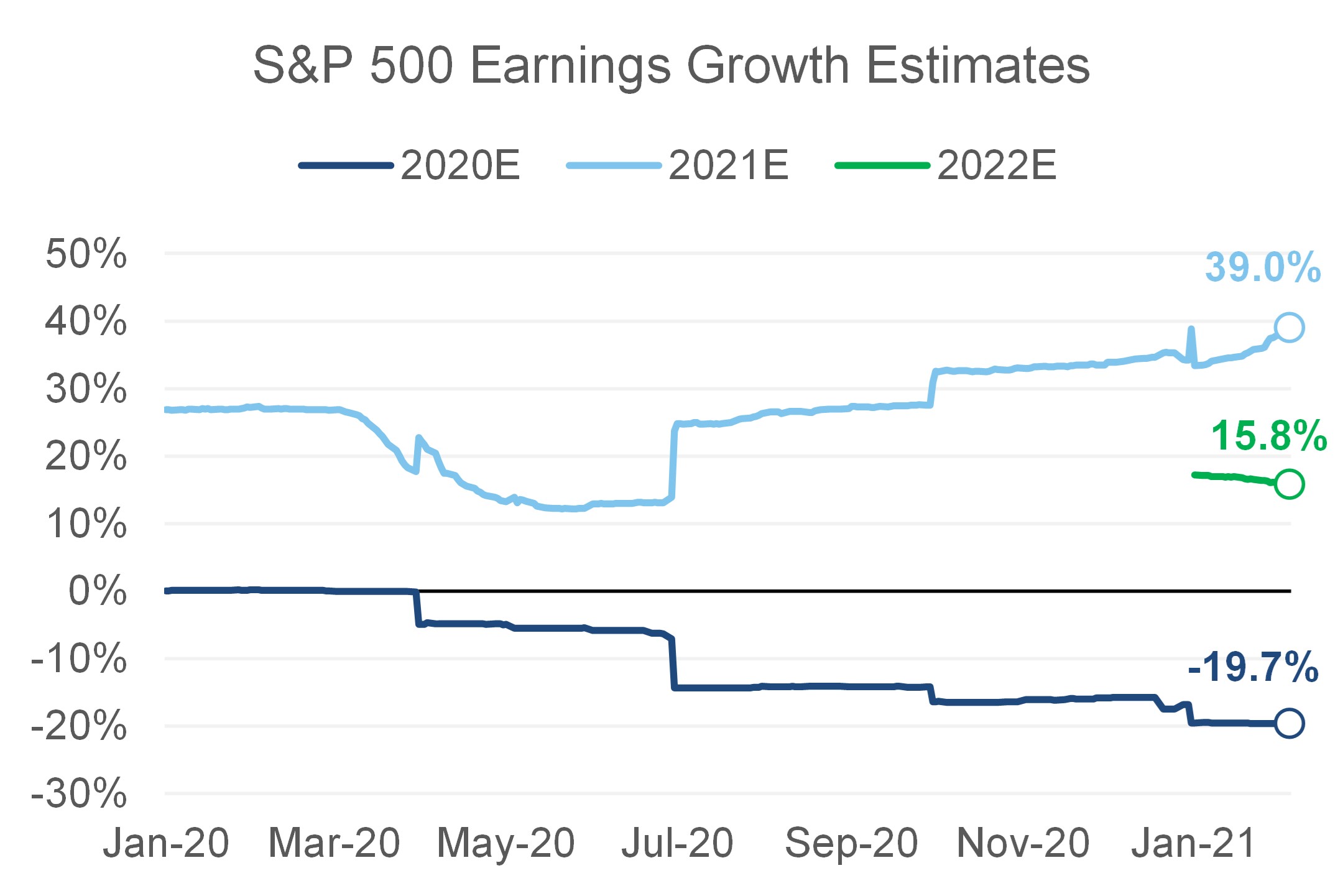

S&P 500 earnings expectations point to a sharp rebound in 2021

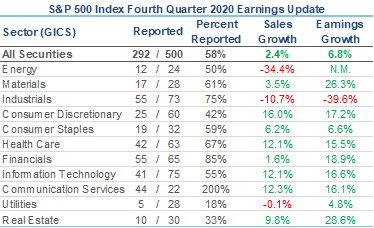

Bloomberg consensus expectations for earnings growth in 2021 have baked in a strong rebound. However, several companies pulled 2021 earnings guidance late last year which means consensus estimates for 2021 could prove conservative. Therefore, we will be seeking clarity as the fourth-quarter earnings season winds down

Market Outlook

Since November, this environment supported typical patterns seen following bear markets, with the advance led by more economically sensitive equity market segments. While we are generally constructive on markets in the near-term, we are keenly focused on the rebound in business activity following more progress with the vaccine. Markets are forward-looking and have benefitted from the reopening optimism, but it remains to be seen how these developments will impact economic data, which is backward-looking. Conditions appear to be in place for growth-sensitive assets to continue their ascent that began a little less than a year ago.

For more information, please contact the professionals at Cedar Cove Wealth Partners.

Footnotes

- DiMeo Schneider & Associates, L.L.C.

- DiMeo Schneider & Associates, L.L.C.

- DiMeo Schneider & Associates, L.L.C.

- DiMeo Schneider & Associates, L.L.C.

The material presented includes information and opinions provided by a party not related to Thrivent Advisor Network. It has been obtained from sources deemed reliable; but no independent verification has been made, nor is its accuracy or completeness guaranteed. The opinions expressed may not necessarily represent those of Thrivent Advisor Network or its affiliates. They are provided solely for information purposes and are not to be construed as solicitations or offers to buy or sell any products, securities or services. They also do not include all fees or expenses that may be incurred by investing in specific products. Past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. You cannot invest directly in an index. The opinions expressed are subject to change as subsequent conditions vary. Thrivent Advisor Network and its affiliates accept no liability for loss or damage of any kind arising from the use of this information.

Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy will be profitable.

THRIVENT IS THE MARKETING NAME FOR THRIVENT FINANCIAL FOR LUTHERANS. Certain insurance and annuity products issued by Thrivent. Not available in all states.

Investment advisory services offered through Thrivent Advisor Network, LLC., a registered investment adviser and a subsidiary of Thrivent. Clients will separately engage a broker-dealer or custodian to safeguard their investment advisory assets. Review the Thrivent Advisor Network ADV Disclosure Brochure and Wrap-Fee Program Brochure for a full description of services, fees and expenses. Thrivent Advisor Network LLC advisors may also be registered representatives of a broker-dealer to offer securities products.